Author: Blue Sky

New Special Expatriate Income Tax Regime for those relocating to France

If you have plans to relocate to France, you may be eligible for very advantageous tax arrangements, subject to certain conditions.

The expatriate tax regime applies to individuals who were not residents of France for tax purposes during the five calendar years prior to their taking up their duties in a company based in France.

Everything you need to know about changes to French Wealth Tax

New rules governing French wealth tax came into effect on 1st January 2018. In this post, we explain what the changes to the law mean if you own a French property or if you are planning to acquire one.

Prior to the changes, French wealth tax (ISF) was assessed on all assets owned by the taxpayer when net taxable assets exceeded a threshold of €1,300,000. The basis for the wealth tax included worldwide assets for taxpayers domiciled in France and real estate assets located in France for non-resident taxpayers.

With effect from 1st January 2018, a new real estate wealth tax scheme (“Impôt sur la Fortune Immobilière” – IFI), is assessed only on the real estate owned by the taxpayer to the extent that the value of the taxpayer’s real estate net assets exceeds a threshold of €1.3 million.

All other assets (especially financial assets) are no longer subject to wealth tax. The five year exemption for property held outside of France for new French residents continues. As with individuals domiciled outside of France, those who have not been domiciled in France during the five years preceding their arrival on the French territory will only be taxed on their French real estate assets, until 31 December of the fifth year following the year of their arrival in France.

The new IFI scheme is governed by the same taxation scale as the former ISF scheme and similar rules as for the French wealth tax apply. More specifically:

- Real estate used in a trade or business are excluded.

- A 30% discount on the value of the taxpayer’s primary residence continues

- Mortgage debts related to taxable real estate assets can continue to reduce the wealth tax base

Mortgage loans as a lever to reduce French Wealth tax

With regards the deduction of mortgage loans in the wealth tax base, new rules specify that interest-only loans will be governed by similar rules as amortising loans. This rule also applies to existing interest-only loans.

For example, a 10 year €100,000 interest-only loan arranged on 1st Jan 2016 will be assessed as follows : for the purpose of reducing the 2018 wealth tax base : €100K – (€100K x 2) / 10 = €80K

French real estate assets with a gross value exceeding €5 million will also be subject to a deduction cap. In practice, when the mortgage outstanding balance exceeds 60% of the property value, the maximum amount of mortgage debt that can be used to reduce the wealth tax base is capped at 50% of the “excess” over and above the 60% cap.

For example, assuming a property worth €6 million with a €4 million mortgage :

60% cap : €6m x 60% = €3.6 m. Excess over the cap : €4m – €3.6m = 400K€. 50% of the excess : 200K€. total deduction from the wealth tax base: €3.8m

As a reminder, assuming the €1.3 million threshold is met, tax bands applicable to net taxable real estate assets are :

Real estate value under €800,000 – 0% tax rate

Real estate value €800,001 to €1,300,000 – 0.5% tax rate

Real estate value €1,300,001 to €2,570,000 – 0.7% tax rate

Real estate value €2,570,001 to €5,000,000 – 1% tax rate

Real estate value €5,000,001 to €10,000,000 – 1.25% tax rate

Real estate value €10,000,000 upwards – 1.5% tax rate

Annual wealth tax bill applicable to unencumbered French real estate assets would be as follows :

| Net taxable assets | Annual tax due |

| 1 300 000 € | 2 500 € |

| 2 000 000 € | 7 400 € |

| 3 000 000 € | 15 690 € |

| 4 000 000 € | 25 690 € |

| 5 000 000 € | 35 690 € |

Early redemption penalties on French mortgages

Most French mortgages come with early repayment fees or penalties also know as ERC. If you have an existing French mortgage and are contemplating remortgaging in France, there are several things you need to be aware of .

Firstly ERCs are capped by law and cannot exceed the lower of 3% of the outstanding mortgage amount or the equivalent of interests paid over a 6 months period.

Besides, under certain circumstances, French lenders are not permitted to charge ERCs. More specifically, ERCs cannot be applied to French mortgages advanced after 1 July 1999 if the redemption of the French mortgage is due to :

1. the sale of the French property and the sale of the french property is correlated with a change of employment

2. the death of the borrower or co-borrower

3. unemployment of one of the borrowers

How to secure the best mortgage deal in France?

Here are a few simple tips to get the best mortgage deal in France. The following recommendations particularly apply to international buyers who can have access to a wide range of mortgage products when buying or refinancing in France.

1. If you can afford the monthly repayments, select a shorter duration for your mortgage contract. In France, the shorter the duration, the lower the mortgage rate.

2. Always factor the cost of the life insurance premium. Lenders will not advance euro denominated mortgages unless a life insurance has been assigned to them. Mortgage insurance is an important cost component of a French mortgage and can represent as much as 25% of the borrowing cost. So make sure to include the life insurance element and don’t simply focus on mortgage rates.

3. Do not go straight to specialist lenders catering for international buyers. They deliver a good service but it can come at a premium cost. Shop around and compare.

4. Negotiate ! In France, fees and mortgage rates are not always set in stone. Bargaining is common place so make sure to challenge the lender. If you are not comfortable pushing back, get a broker to do the negotiating on your behalf.

5. It’s location, location, location but not rates, rates. To get the best mortgage deal, always include fees (completion fee, early redemption fee) and the cost of the guarantee that the lender will require. Fixed fees can make a big difference to the overall cost of a French mortgage.

6. If you want to have access to the whole of the French mortgage market, use an authorised French broker. Make sure that the mortgage broker is regulated to arrange mortgage contracts in France and make sure that the broker can also arrange life insurance contracts. A French mortgage broker has a best advice duty and cannot charge fees before completion.

For further information, make sure to contact us.

French mortgage insurance : switch and save?

Mortgage protection insurance is mandatory when taking out a mortgage in France. The majority of French lenders require that borrowers are insured for the amount of the loan through a life insurance policy which is assigned to the lender.

With mortgage insurance premiums accounting for as much as 30% of the total borrowing costs, it pays to shop around and switch. French banks offer block insurance policies which tend not to be as competitive for younger or senior borrowers. A qualified and regulated mortgage and insurance broker will be able to provide you with tailored advice.

Buying a property in France

Principles applicable in French property law go back to the declaration of human and citizens’ rights in 1789 “the right to property is an inviolable and sacred right, that no one can be deprived of …”

In addition to protecting property owners, the French legal system has, over the years, added a number of laws designed to protect the buyer and, as such, creates a very safe and heavily regulated purchasing environment.

Initial Stages

After a property has been found and a purchase price has been agreed, the vendor and the buyer must sign an initial contract – known locally as the Compromis de Vente. In some cases, this document will be a standard contract held by a French estate agent; however, it can also be drawn up by an official of the government – referred to in France as a Notaire.

Once the Compromis de Vente has been signed by all parties, a seven-day cooling-off period begins. During this seven-day period, the buyer has the opportunity to withdraw from the purchase. After the cooling-off period has ended, the transaction becomes legally binding, and significant penalties are payable if either party should withdraw from the sale.

A conditional clause can be added to the Compromis de Vente stating that the purchase is subject to the mortgage application be approved by at least one lender.

A deposit of at least ten percent of the purchase price will normally be required – although it will remain in escrow with the notaire until the transaction completes successfully. In the event that a mortgage application is not approved, the compromis de vente becomes void and the deposit is refunded.

At this point you may wish to appoint your own notary to oversee all aspects of the transaction.

The appointment of your own notary does not incur any extra costs.

Role of the Notaire

The involvement of a notaire in real estate transactions is a legal requirement in France. He is a public official who has a monopoly over conveyancing. One notaire can be appointed to oversee the entire transaction; however, both the vendor and the buyer can appoint their own. The notaire will oversee all aspects of the sale to ensure all applicable laws are adhered to and that all taxes are paid. The notarial profession is strictly controlled by statute owing to the delegation of public authority. The profession is also monitored closely by its peers and if necessary by the judicial authorities.

A notaire will typically charge between six and eight percent for their services, and all fees are payable on completion of the sale. For the most part, notary fees are taxes set by the Government.

Conveyancing process

The average timescale for completion of the various searches and legal checks – undertaken by the notaire – is three to four months. A meeting will then take place between the buyer and vendor – or parties nominated to represent them by proxy. The final deed of sale – known in France as the Acte de Vente – will be signed during this meeting, and the property’s ownership will finally pass to the buyer.

Property Prices in France

The French housing market is expected to strengthen further in 2018. Strong demand for houses in France is buoyed by low interest rates. Find out more about the latest trends in French property prices.

Bank account and currency transfer in France

As your mortgage instalments will be debited from an account by Direct debit, you will need to open an account with a bank in France. Bluesky Finance can help you find a suitable retail bank and the right package for you.

Save money on your international transfers

Bluesky Finance has teamed up with Moneycorp to save you money on international money transfers. Whether you’re buying property overseas, emigrating or sending money to friends and family, Moneycorp can make sure your money gets to where you need it at a great rate, for a low fee and with all the help you want.

By using Moneycorp you will benefit from:

• Bank beating exchange rates

• Fast online money transfers 24/7

• Free expert guidance at the end of the phone

• Safeguarded customer funds

Sign up FREE and save money today with Moneycorp. Registering with Moneycorp only takes a few minutes – it is completely free and carries no obligation to use the service.

Open a free account here

Sale and rent back – French Properties

Sale and rent back is a facility where owners of French properties sell their properties for cash and maintain the right to remain as tenants for up to five years with an option to purchase the property back.

Sale and Rent Back can be an appropriate solution for owners and landlords

- who want to achieve a quick sale

- who have fallen behind their mortgage payments

- who need to repay or consolidate debts or late taxes

- need to raise finance for business or property investment purposes

- who manage a Buy to Let portfolio

- and who want to maintain the right to use or let the property

We have access to a panel of institutional investors who can arrange sale and rent back schemes. Feel free to get in touch to find out whether a sale and rent back scheme can be the right solution for you.

Capital Gains Tax in France

Tax Overview

Capital gains tax – impôt sur les plus values – is a tax payable in France on gains arising from the sale of land or properties. Capital gains are calculated as the difference between the sale price and the purchase price or the value that was reported when the property was received as a gift or by inheritance. Rules governing capital gains tax vary in accordance with the sale price, the nature of the asset, the country of residence of the seller and how long the asset has been held. Capital gains made on the sale of assets are exempt when the sale price is under €15,000. Sale of a principal residences are totally exempt, regardless of how long the property had been owned. Capital gains achieved on properties sold when the property has been owned for 30 years or more are also exempt. In other cases, the vendor is liable to pay tax and social security charges (CSG, CRSG) on the net capital gains.

To calculate the amount of net capital gains, Gross Capital Gains can be adjusted by the following factors:

Deductible expenses

Home improvement expenses (extension, double glazing, new kitchen etc) are deductible from the sale price as long as the vendor has kept invoices and proofs of payments and has not already deducted these expenses for other purposes. Alternatively, the vendor may use a flat rate deduction equal to 15% of the purchase price. To be eligible, the vendor must have owned the property for at least five years. Sale fees can also be deducted from the sale price. These may include the costs incurred to complete the mandatory certificates and surveys (eg Energy Performance Certificate) as well as the fees the fiscal representative may charge.

Purchase fees

Fees including stamp duties, notary and agent fees which were incurred when buying the property can be added to the purchase price. By default a flat rate of 7.5% of the purchase price can be used.

Taper relief

This is effectively an allowance for the duration of ownership.

Taper relief for tax purposes:

6% for the sixth to the 21st year of ownership;

4% for the 22nd year

Taper relief for social charges purposes:

1.65% for the sixth to the 21st year

1.60 % for the 22nd year

9% for the 23rd to the 30th year

Tax and social security rates :

Income tax rate applicable to Capital Gains Tax stands at 19%

In addition, social charges of 17.2% apply to Capital Gains Tax.

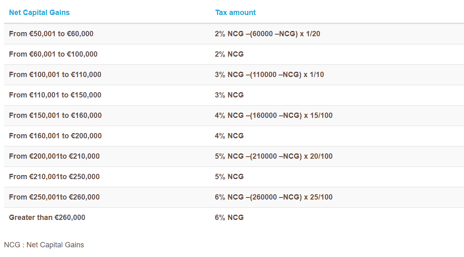

Additional taxes are also levied when net Capital Gains are greater than €50,000. Additional taxes payable are calculated as follows: